Morgan Stanley has recently published the report with the results of the 2021 watch market. In the previous year, that of the beginning of the pandemic, we had seen how the market had particularly blamed the health crisis with a -21.8% turnover business, but bringing home some significant results (you can read the previous report here).

On the other hand, 2021 ended with interesting results, with Audemars Piguet surpassing Patek Philippe in turnover for the first time, while Rolex, Cartier and Omega remain on the podium but with Cartier climbing to second place.

Let’s now analyze these results in detail, also referring to the very detailed article by Oliver Muller from Le Temps.

A glimpse of the whole industry

The eleventh-century watch industry recorded an all-time high of CHF 22.3 billion in 2021 (CHF 21.2 billion for wristwatches alone).

The first thing to note is that we have returned to the level of pre-Covid sales with a result up 31.2% compared to 2020 and even 2.7% compared to 2019.

The interesting thing, however, is that the growth in turnover does not correspond to a growth in terms of units sold which instead amounted to -4.9 million compared to 2019. This means that the increase in turnover is mainly due to an increase in prices. , which can also be linked to the significant inflation that has hit the world economy in recent years.

Let’s leave these general results and dive right into the ranking now!

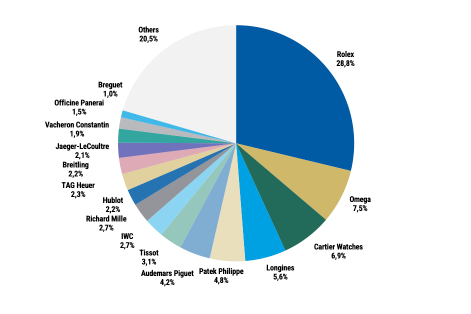

The podium by turnover

With 29% of the market share of the Swiss watch industry and an estimated turnover of 8 billion in CHF, Rolex remains the market leader. On the second step of the podium we find Cartier with 2.39 billion francs, which corresponds to a growth of 40% in one year. Omega drops a step with sales of 2.2 billion francs but also grows by 30%.

At this point, however, we want to focus on some considerations to frame the situation. It’s true, Rolex’s turnover exceeds that of the entire Swatch Group by 1 billion and that of Audemars Piguet or Patek Philippe by almost five and a half times.

However, we must not forget that Rolex has sold a whopping 1,050,000 watches. That means 1,000,000 more watches than Audemars Piguet and 980,000 more watches than Patek Philippe. Even compared to Omega, the production of Rolex is almost double.

Proceeding in the ranking, just off the podium we find Audemars Piguet, Longines and Patek Philippe with 1.5 billion Swiss francs in turnover. Clearly, even though the turnover is similar, the units sold are not. While Audemars and Patek have sold 45,000 and 68,000 units respectively, Longines reaches 1.8 million units.

The podium by average retail price

We thought it would be very interesting to present you a ranking according to the average sales value per single unit. Based on this factor, the circumstances change.

In first place we find Richard Mille, with an average price per unit (PPU) of 226,000 CHF.

In second place, on the other hand, we have a complete reversal rollover. F.P. Journe, last in the ranking based on turnover (remember the extremely limited production), has an APM of around 59,000 CHF and 900 pieces produced.

Sul gradino più basso del podio invece troviamo A. Lange & Sohne che con un fatturato di 210 milioni di CHF e 5.000 unità vendute presenta un PMU di 42.000 CHF.

A predominantly polarized industry

Certainly, in recent years there has been an increase in sales especially for a small circle of elected brands, which seem to attract the attention of the public more than others.

Behind the club of 4 brands that have shown substantial growth for several years (Rolex, Audemars Piguet, Patek Philippe and Richard Mille) can be added a second group made up in particular of Cartier, Omega, Longines and IWC.

The 5 most important brands represent more than half of the market (53%), 13 brands conquer a market share of 75%, 25 brands occupy 90% of the market. These figures should be compared with 350 Swiss brands in business.

However, it must also be said that the luxury watch market is very jagged in terms of brand commercial choices. Many houses purposely keep ultra-limited productions to appeal to a very small circle of loyal customers and do not show the need or desire to grow in terms of sales or turnover. This makes the industry seem even more polarized than it really is.

The Audemars Piguet strategy

Definitely worth noting is the variation in Audemars Piguet’s strategy in recent years.

The Maison of Le Brassus has achieved a record year, the best in its history. It surpasses its historic competitor Patek Philippe, which despite its successes in the esteem and the buzz created by the collection of its legendary Nautilus 5711, does not live the same virtuous dynamic as AP.

However, Audemars Piguet is mostly sailing on the uninterrupted wave of the success of its Royal Oak, which this year celebrates its 50th anniversary and which will undoubtedly help make 2022 another record year but which may not be enough in the long run. absence of new collections worthy of the Maison.

According to Oliver Muller, it can be estimated that almost 90% of its sales are due to its most iconic product (Royal Oak and Royal Oak Offshore). The Code 11:59 collection launched in January 2019 is starting to make its way and is generating 5% of the brand’s sales.

Note, in terms of strategy, is the relationship between direct sales and reseller sales. In fact, following a sharp reduction in authorized dealers and the opening of AP Houses and Boutiques, the brand produces 72% of sales through direct channels and only 28% from authorized dealers. The advantages of such a strategy are mainly found in capturing a higher margin than previously granted to the retailer and having a direct relationship with its customers without intermediaries.

The big watchmaking corporations

The large corporations Richemont, Swatch Group and LVMH certainly deserve a separate discussion. For Kering we limit ourselves to underlining that, after the buyout of Girard Perregaux and Ulysse Nardin which had been a failure until now, the company maintains a watch division only for Gucci.

Richemont

After a particularly difficult year for the group, 2021 turns out to be a great success. Cartier is the clear leader with sales of CHF 2.39 billion.

The winners of the recovery in 2021 are also Vacheron Constantin with + 53% on turnover and Hermès, which achieves a performance of + 73%, even if the turnover of 364 million CHF places it only in 19th place.

Swatch

Swatch Group had a great year with a plus of 30.7%. What is worrying according to Morgan Stanley is the acceleration of Rolex compared to its main challenger Omega, whose market share (7.5%) corresponds to a quarter of that crowned.

To underline in this case, however, is the sensitively different commercial strategy of Rolex, aimed at increasing desirability and a not very natural difficulty in finding the timepieces that in our opinion certainly rewards in the short term but which could backfire in the long term once. that consumers will have grown tired of these games.

LVMH

Not even LVMH can fully celebrate. Despite Hublot’s growth of + 45% and an excellent result in terms of sales also by Zenith, the group is losing market share.

Independent watchmakers and their growth in 2021

If you’ve been following IWS for a long time, you know we like independents a lot and have been targeting them since the very beginning. Although the Morgan Stanley ranking is not fully understood, the niche brands are enjoying unprecedented success. Social media certainly play a role of primary importance by making accessible to the public what was previously restricted to a very limited circle of enthusiasts.

Conclusions

At the end of this journey, the picture is clear enough. It is dominated by a few brands that are widely desired and inaccessible. However, a general positive trend is confirmed for the entire industry, due in part to the disastrous past year, as well as the undoubted increase in popularity of the goods we love so much.

After analyzing the past year, all that remains is to ask: What will happen in 2022?

For all the news in real time, follow our Instagram profile.