New year, new Morgan Stanley Swiss Watch Industry Report. Here we are again to analyze the annual summary of the state of the Swiss watch industry compiled by Morgan Stanley and LuxeConsult, a consulting firm on the watch industry, founded by Oliver R. Muller.

Just like every year, we’re here to bring you the most salient parts of this report. If you want to compare with previous years, here is the link to the report articles for 2020, 2021, and 2022. For the first time, we also offer you the entire ranking by Morgan Stanley and LuxConsult, which you can find at the end of the article.

The Swiss Watchmaking in 2023 at a Glance

The trends observed over the last three years continue unabated. The premium factor and the polarization of sales continue to dominate within a market that increases in economic value but decreases in terms of volumes.

If in 2022 the value of the export of finished watches of the Swiss industry reached CHF 23.7 billion, in 2023 it reached CHF 25.5 billion (+7.6%), marking a new historical high. Certainly, this increase was partly driven by higher than normal inflation, but even taking into account a YoY inflation of 6% in December 2023, the result would still be positive. Retail sales also surpassed every new previous record reaching CHF 50 billion (+4.2%), a more modest result, also influenced by the monetary fluctuations of the Swiss franc against other currencies. This year the increase in volumes was definitely more marked compared to 2022, reaching 16.9 million units sold (+6.96%). Such a marked increase that, except for the particular post-Covid year, we can only find going back to 2012.

Regarding the competition, the trend of polarization we have witnessed has strengthened. Patek Philippe, Omega, Cartier, and Rolex alone hold 50.2% of the market share. An incredible fact to consider is that Rolex alone (excluding Tudor), holds 30.3% of the market share, still an increase compared to 2022.

The Top 10 by Revenue

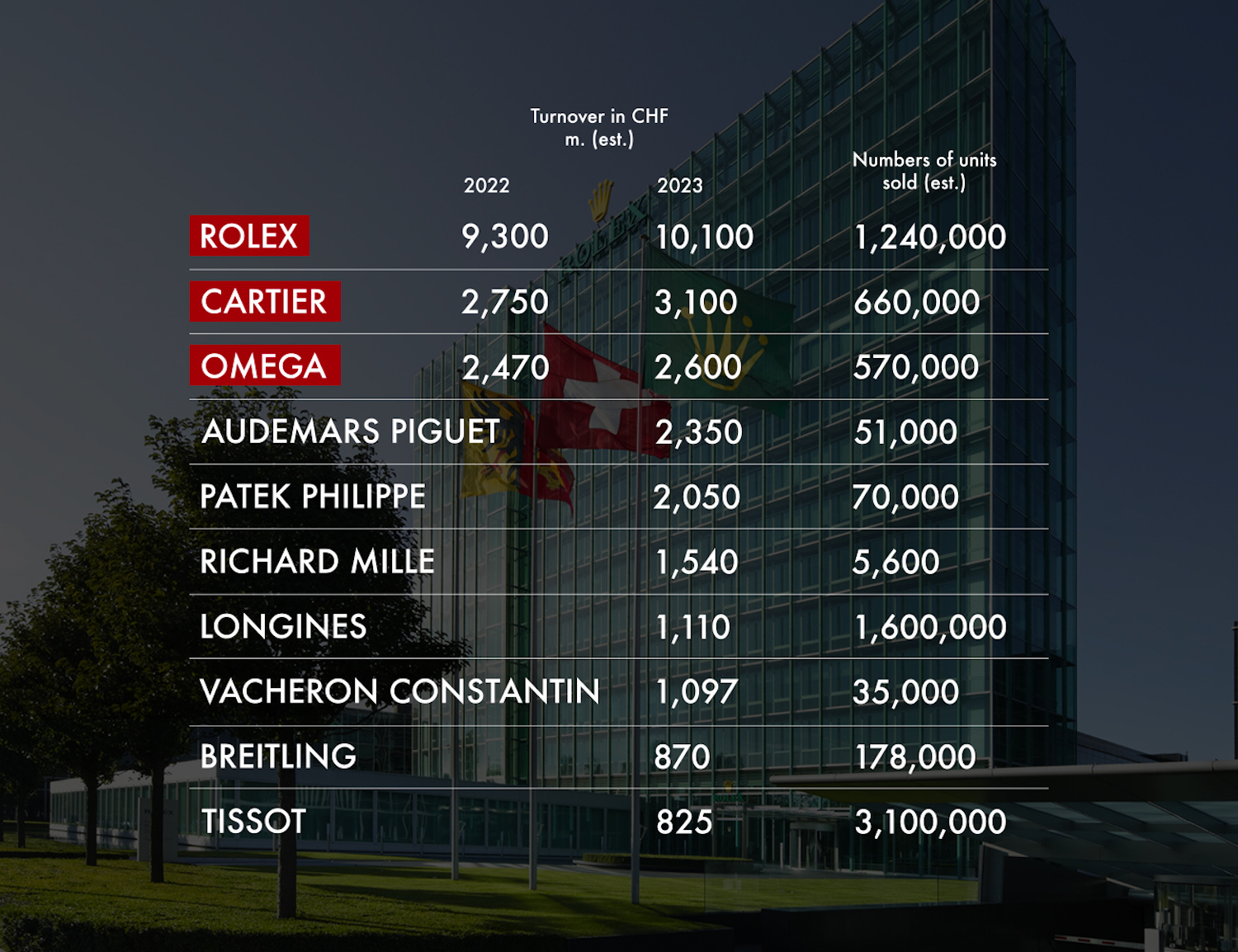

On the podium this year again we find Rolex, Cartier, and Omega, respectively in first, second, and third place. Rolex remains firmly in the lead and for the first time in history surpasses 10 billion CHF, maintaining about 1.2 million watches sold. If the situation for Cartier and Omega was more balanced, now Morgan Stanley estimates a gap of Cartier reaching 3.1 billion CHF (+15%), while Omega records a slower climb to 2.6 billion compared to 2.47 in 2022.

Immediately below the podium, we find the new trinity unchanged. Audemars Piguet remains in fourth position, Patek Philippe in fifth, and Richard Mille in sixth. Audemars consolidates its position reaching 2.3 billion CHF in revenue (+10%). Patek Philippe reaches for the first time 2 billion in revenue. Richard Mille reaches a turnover of 1.540 billion CHF; an incredible +18.5% compared to 2022. The three brands, in order of position for revenue, produce respectively 51,000, 70,000, and 5,600 watches. The average selling price of Richard Mille continues to increase and reaches 275,000 CHF per sold watch.

In seventh place, we find Longines again this year. According to Morgan Stanley, already coming from a particularly challenging 2022, the brand continues to record a decrease in its turnover, albeit to a lesser extent than the previous year. The reason is probably to be found in the excessive exposure on the Chinese market which also this year struggled to recover.

In eighth position, we have the newcomer to the Billionaires Club, Vacheron Constantin, with an increase of almost 20% on sales. An incredible performance, partly driven by the policy dictated by Audemars Piguet and Patek Philippe that VC has successfully emulated.

Morgan Stanley estimates Breitling in ninth position also for this year, standing at a slightly higher turnover. Therefore, a slight reduction in growth for a brand that until this year had recorded exceptional results.

In the tenth position of the Top 10, we find a surprise with an average price of about 409 CHF. Tissot, after its poor performance in 2022, a year in which it lost four positions, managed to regain two, bringing it back into the top 10. Morgan Stanley attributes the merit to the success of the PXR collection.

Big Groups

As we said, also in 2023 the polarization continues and the industry is configured as a sort of oligopoly. Swiss watchmaking is in the hands of four main groups that together hold 75.9% of the market share by retail sales value. We are obviously talking about Rolex, Swatch Group, Richemont, and LVMH.

However, we must note how this year the trend has slightly reversed. Indeed, to keep above the 75% conglomerate, is the good performance of Rolex, the other three groups have lost more or less significant market shares in favor of other market players, particularly towards the trinity AP, PP, RM which have recorded a significant increase of almost, or more, than 100 basis points each.

Rolex

The leader in this case is Rolex (with Tudor), which achieves 32% of market share. This, too, is data growing compared to the previous year by a good 1.5 percentage points. Of the group, 95% of sales are attributable to the Rolex brand while the sister Tudor represents only a meager 5%. If in 2022 Tudor had recorded a very positive year (+11%), this year it did not go that way. The company, in fact, saw its turnover decrease (-4%) for the first time since 2017. The general trend of the group seems to be unchanged, a down-selling towards Tudor due to a lack of Rolex products to increase the brand’s desirability. However, this strategy highlights its shortcomings when Rolex products start to become more accessible with the reduction of waiting lists, probably the drop in turnover is a symptom of this.

The average selling price for Rolex continues to rise and reaches 12,220 CHF, testifying that the higher volumes occur in its core collections in steel and steel and gold (Submariner, GMT, Explorer, Daytona). There is still a trend of distancing from Omega, which until a few years ago could be considered the brand’s main competitor. Now, in fact, the average selling price of the crowned house reaches double that of the counterpart, highlighting significantly different strategies.

Swatch Group

In second position with 19.4% of market share, Swatch Group continues the negative trend already started in 2022, a year in which the group had obtained according to Morgan Stanley market shares of 19.8%. The main driver of this result continues to be the excessive exposure of the brands to the Chinese market, which this year has recovered much more slowly than expected. In Swatch Group continues the unstoppable ride of the Swatch brand which, thanks to the Moonswatch operation, after recording an increase in turnover of 87% in 2022, reaching about 400 million CHF in turnover, now touches 660 million.

In addition to the high dependence on the Chinese market, Morgan Stanley also highlights an excessive polarization within the group. In fact, Omega alone is responsible for 60% of the entire group’s operating margin. However, the Report also notes how this is a trend common to the big luxury groups where Cartier, Gucci, and Louis Vuitton play the same role respectively for Richemont, Kering, and LVMH.

Richemont

According to Morgan Stanley, this year Richemont experienced a rather mixed year. On the one hand, brands like Van Cleef and Vacheron Constantin performed well, on the other hand, the negative performance of IWC which records a turnover contraction of -13% is alarming. Probably, says Morgan Stanely, the reason is to be found in an overly ambitious price positioning. In general, Richemont closes the year losing market shares, going from 19.4% to 18.7%, moving away from Swatch Group.

LVMH

The LVMH group ranks fourth in the “Groups” ranking with market shares equal to 5.8%. The main brands of the group, according to Morgan Stanley, have seen their turnover contract quite significantly. Hublot arrives at 670 million CHF, against 744 in 2022, while Tag Heuer goes from CHF 729 million to 615.

Here, we allow ourselves a small digression. Such a reduction in Tag Heuer’s turnover seems to us strongly incompatible with the mix of products and the intense marketing activity that has been carried out in the last year. The new Carrera collection is one of the best products launched by the brand in the modern era, probably it will take a few years before this can bear its fruits.

Continuing with the brands of the group, Bulgari records another very positive year reaching 445 million CHF in turnover (+20% compared to 2022). Even the newcomer Louis Vuitton and the historic Zenith record positive results with a +24% and +14% on the turnover of 2022. However, these are still figures too low to be able to concretely influence the position of the entire group.

Big Independent Brands

According to Morgan Stanley, this was the year of the independents. Actually, we have been talking about it for a while. We will proceed from here on talking about independent brands, using the definition given by Morgan Stanley: a brand that does not belong to any luxury sector group, and that is neither listed on the stock exchange nor institutionalized.

We, allow ourselves to insert a further difference, between large and small independents. So now we will talk about the big independents and later we will focus on the small ones.

Breitling

After the stellar performance of 2022, Breitling slows its ascent recording an increase of only 10 million CHF, reaching 870 million.

Hermès

From 2010 to 2018 Hermés saw a significant slowdown of its watch division, but those days are now gone. From that year onwards, in fact, the company’s department has seen an impressive growth of +72.5%, +43.1%, +13.8% in 2021, 2022, and 2023 respectively. Now the turnover stands at CHF 593 million, against 519 million in 2022.

The main merit is the concentration by the company on products that maintain the brand’s characteristic DNA attentive to aesthetics, without compromising on the quality of the purely mechanical and watchmaking part. This commitment has also been widely recognized last year by the Grand Prix D’Horlogerie, which awarded the brand two prizes. The company in this perspective has also pushed itself in increasing the price of its watches positioning them at a higher level. It must also be remembered that thanks to the lever of incredibly desired bags, watches present an important down-selling opportunity.

Chopard

The performance of Chopard has been fluctuating in the medium term. The brand continues to bounce between the nineteenth and twentieth position in the ranking by revenue. Despite this, in 2023 the company recorded sales of 420 million CHF, compared to 410 million in 2022 and 369 million in 2021. In our opinion, given the success of the Alpine Eagle collection and the commitment in the company put in these last years, the results can be even better in the near future.

At this moment the company is producing very interesting models in the L.U.C. collection highly appetizing for most collectors.

Small Independents

Ulysse Nardin e Girard Perregaux

Although both part of the Sowind group, we want to consider them as independent realities for this time, as they have recently come out of the sphere of influence of a true big group: Kering. The positive effect of the buy-out seems to have slowed down, but the trend remains broadly positive.

H. Moser & Cie.

Moser is known for its essential timepieces without a logo and for its bold and very unconventional marketing. This year the brand enters the Report for the first time with a turnover of CHF 93 million and an average price of CHF 36,000. Moser’s entry into the Report is a testament to how these realities are becoming important for the watchmaking industry in a narrower sense, as well as for collectors and common opinion.

F.P. Journe

Further new entry is F.P. Journe, with its turnover of CHF 98 million, only 1,800 watches sold and an average price of over CHF 75,000. Journe watches are positioned among the most sought-after and desirable objects for collectors around the world thanks to the skill with which the brand combines tradition and classic forms with highly innovative and aesthetically appealing expedients.

Parmigiani

Parmigiani, another small independent brand was already present in 2022, in 48th position, with a turnover of CHF 44 million, 1,800 units sold and an average price of CHF 37,000. This year the brand, continuing successfully in its renewal policy has recorded exciting results bringing the turnover to CHF 66 million and 3,000 watches sold maintaining an average price of about CHF 35,000. It is an incredible brand that in recent years has produced one masterpiece after another. Soon Italy will be able to know it better in person.

Greubel Forsey

With a turnover of just 50 million CHF and the lowest number of watches sold in the entire Report (only 255 pieces) Greubel Forsey ranks as a newcomer in 50th place. A brand with incredible savoir-faire that thanks to its spirit of innovation and skill in building three-dimensional dials with a distinctive appearance allows it to dethrone Richard Mille from the throne of the highest average selling price, reaching the impressive figure of CHF 330,000.

The Complete List

Visit our Youtube channel to experience the best of the watchmaking world firsthand.

For all real-time updates follow us on Instagram.